SpaceX Update: Houston, We Have An IPO

That's one small step for man, one giant leap for mankind. - Neil Armstrong

Elon Musk’s bankers are in the room right now pitching the most anticipated IPO since the internet was young.

The roadshow started today, June 4.

Pricing is expected June 11.

Listing is likely June 12.

On June 3, Space Exploration Technologies Corp. (ticker SPCX) announced they will begin trading on the Nasdaq at a fixed price of $135 per share, raising $75 billion and landing with a $1.77 trillion valuation. To put that in perspective: that is larger than Saudi Aramco’s 2019 record-breaking IPO and would place it as the 7th largest listed company in the US, ahead of … wait for it… Tesla!

You have already read the headlines so we are not here to repeat them. Here are the five things that I think matter most, each one connecting back to something we have already explored together in my substack posts from days gone by.

The Market Joins Whether It Wants To or Not

This is the part most retail investors are not thinking about and it may matter more than the IPO price.

Nasdaq changed its "fast entry" rules on May 1, 2026. Any newly public company ranked in the top 40 by market cap qualifies for Nasdaq-100 inclusion after just 15 trading sessions, with the minimum float requirement eliminated entirely. FTSE Russell followed suit with its own fast-entry rules. SPCX will rank as the 7th largest company in the Nasdaq-100 on full market cap weighting (just ahead of Tesla) putting it above every other constituent except Nvidia, Apple, Alphabet, Microsoft, and Amazon.

Then, the day the roadshow opened S&P Global announced it would not change its requirements for entry into its major indices, effectively blocking SpaceX from swift S&P 500 inclusion. The stated reason: "exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization." In plain English: SpaceX posted a net loss of $4.94 billion in 2025, and S&P rules require GAAP profitability in both the most recent quarter and across the trailing four quarters combined. SpaceX does not pass that test. S&P also left its 12-month seasoning period and its 10% minimum float requirement in place -- and SpaceX's IPO represents fewer than 5% of shares outstanding. The S&P 500 door stays shut for at least a year, possibly longer if the AI segment continues to burn cash. S&P did modify entry rules for its broader S&P Total Market Index and Dow Jones U.S. Total Stock Market Index, creating a limited pathway for SpaceX to join those less widely followed indices.

One important nuance on the Nasdaq side: initial weighting will be based on float (shares actually available to trade), not full market cap. At listing, SpaceX's float is approximately 555.6 million Class A shares -- the IPO shares only. That is roughly 4% of total shares outstanding. On a float basis, SPCX enters the Nasdaq-100 at roughly the weight of a Netflix or Qualcomm -- significant but not index-altering on day one. As lockups expire and float expands through the staggered release schedule, the weighting climbs toward that full-cap 7th-place figure, mechanically forcing passive Nasdaq funds to buy more shares over time.

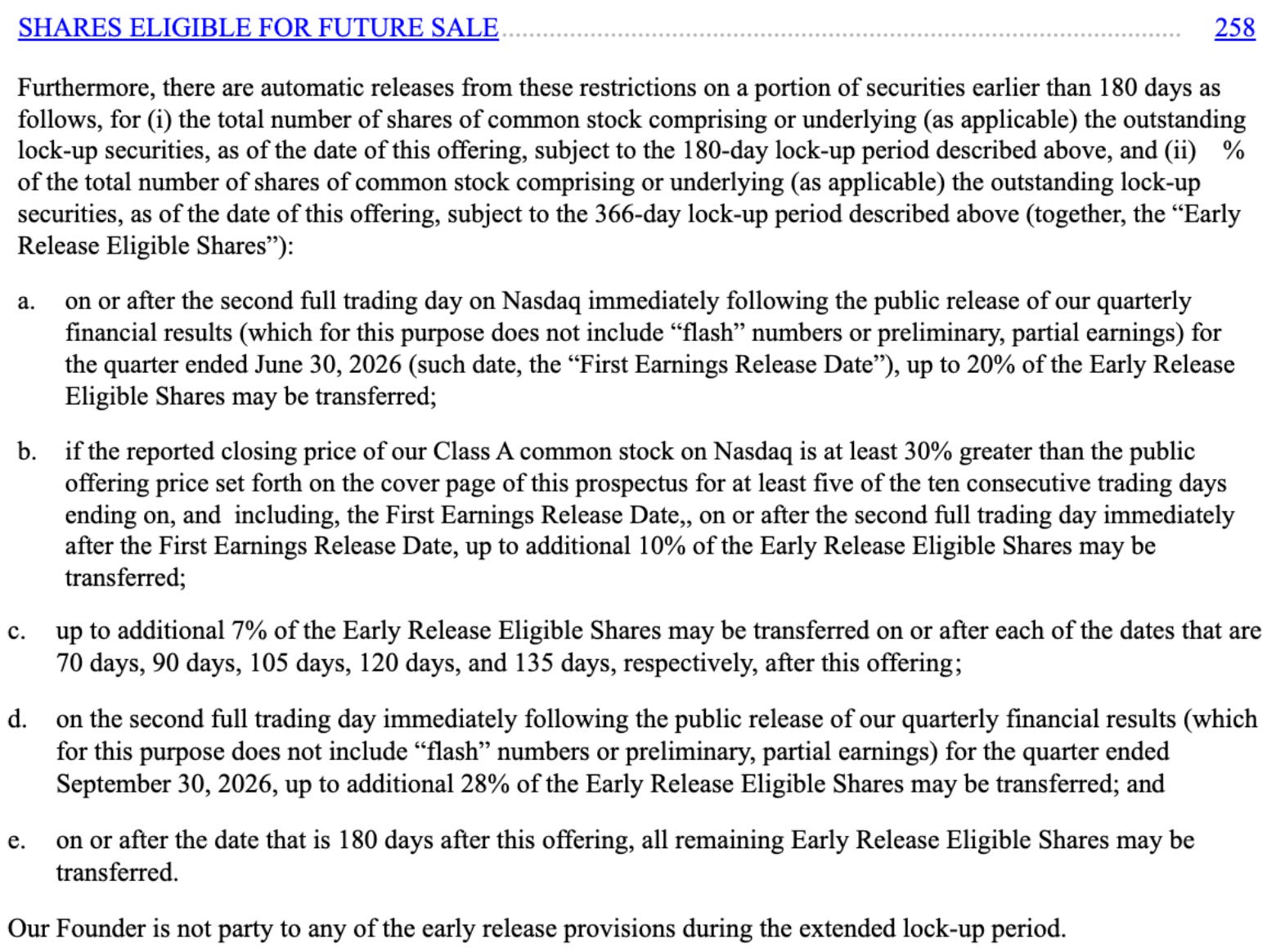

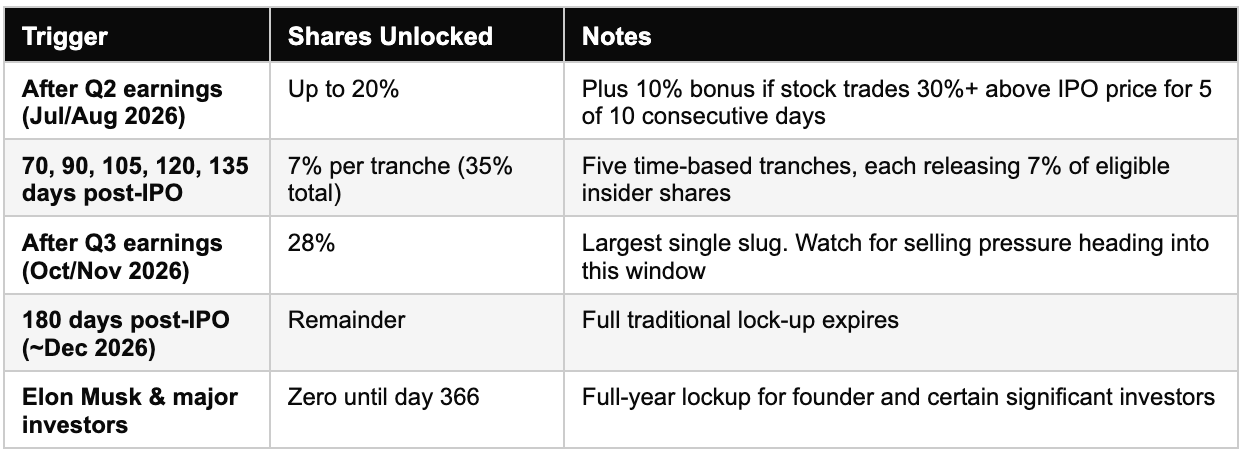

Now, the lockup structure is genuinely novel and worth understanding. From the S-1:

I have summarized it in the table below:

The good news: there is no single cliff and the supply shock is smoothed.

The honest news: there is a rolling six-month overhang.

Retail investors who rush in on day one are buying ahead of sustained insider liquidity. History is unkind to those trades.

What that means for you: if you own a Nasdaq-100 ETF, an S&P 500 index fund, or virtually any broad-market passive strategy, you will own SpaceX whether you want it or not. The index brings it to you and it is likely to be buying more of them as the lock-up expire.

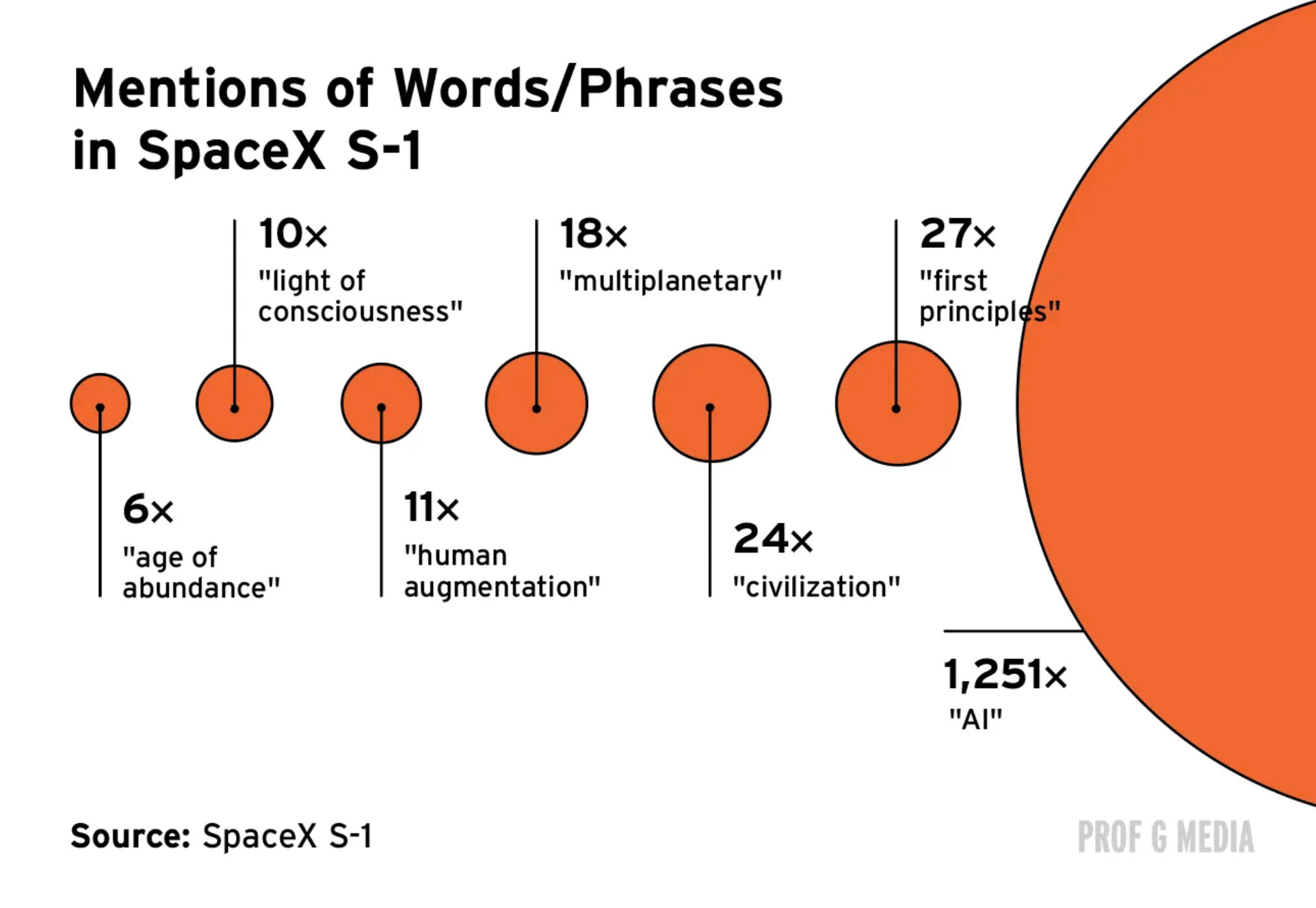

The S-1 Word Count Tells You Everything

The image below (Source: Prof G Media) is not a joke, rather it is a diagnosis.

A prospectus is a legal document, but also a sales document. The SpaceX S-1 manages to be both, while occasionally reading like a manifesto for the human species. A few highlights from the filing:

“We believe we have identified the largest actionable total addressable market in human history... to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars.”

SpaceX S-1, Prospectus Summary, p.1

“We do not want humans to have the same fate as dinosaurs.”

SpaceX S-1, “Why This Matters Now,” Prospectus Summary, p.7

“We are capable of better understanding the universe, exploring the universe, and ultimately making life multiplanetary across the universe. We are becoming a civilization with the ability to reach beyond Earth’s cradle and begin to inhabit other worlds.”

SpaceX S-1, “Why This Matters Now,” Prospectus Summary, p.7

This is not an outright criticism. I’ve written before how to read a quarterly earnings report and watch for certain red flags in Episode 15. Elon Musk has earned the right to dream big in a prospectus. It’s worked for him before and has propelled him to become the richest man in the world, well before this IPO. His vision has repeatedly become the product. But here is something to consider: when a company’s S-1 reads more like a TED Talk than a 10-K, it is worth asking exactly what is doing the work. Is it the business? Or is it the story? For now, the story is carrying a premium the business has not yet fully earned. That gap doesn’t mean the stock will crash back to earth (pun intended). It is however, worth highlighting before you write the check.

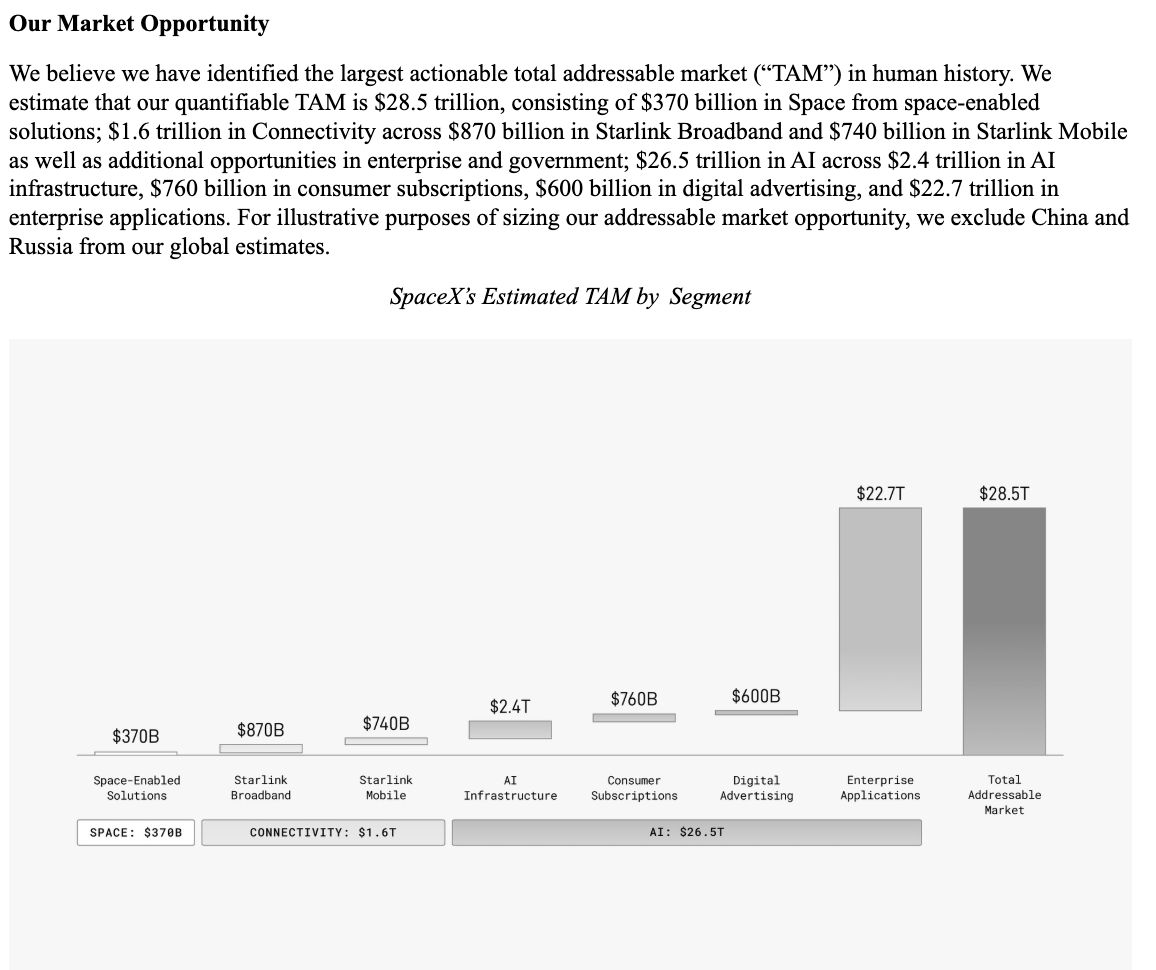

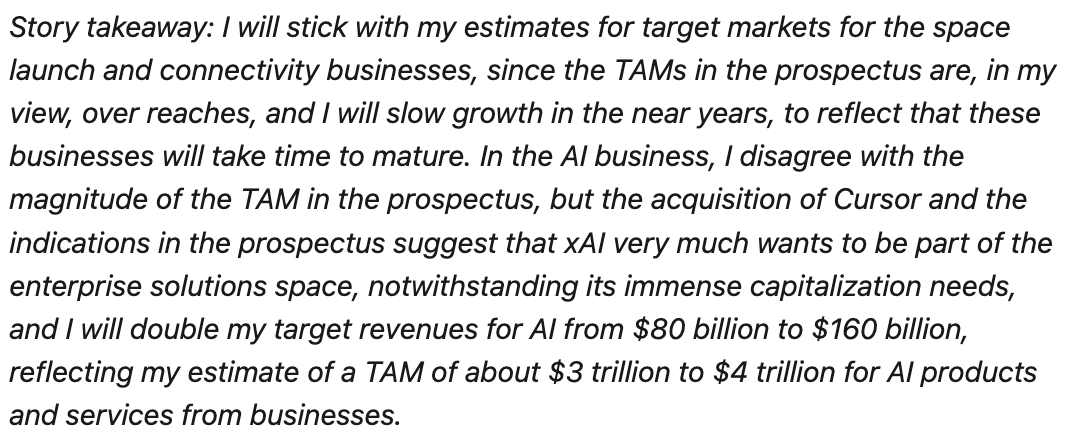

The Largest TAM in Human History (Their Words, Not Ours)

In Episode 19 of LIT, we built the entire framework for how to read a TAM claim. Why it matters, how to interrogate it, and why getting the TAM right often matters more than picking the right company within a wave. That episode was built around SpaceX as the teaser and now we have the actual numbers.

The S-1 dedicates a full section to this (see: “Business” p.130 of the filing). The headline number: SpaceX claims a total addressable market of $28.5 trillion, which the company describes as “the largest actionable TAM in human history.” For context, that is slightly smaller than the US GDP and roughly the combined annual GDP of China, German and Japan (numbers 2-4 respectively).

The number that stops you in your tracks: $26.5 trillion of the $28.5 trillion TAM (or 93%) comes from AI. A business that did not exist inside SpaceX before February 2026, when the company absorbed Elon’s AI startup xAI. The rocket company’s TAM is almost entirely AI.

The S-1 itself acknowledges this tension. In the risk factors section (p.26), the company flags: “The estimates of future market opportunity and forecasts of market growth, and our ability to capture such markets, included in this prospectus may prove to be inaccurate.” The McKinsey projection for the broader space economy is $1.8 trillion by 2035, real growth, but a different order of magnitude from $28.5 trillion. Damodaran in his valuation piece states: “This estimate borders on fantasy, but I will cut the bankers who came up with these numbers some slack”. So he comes up with this:

None of this makes the TAM wrong however. If the wave breaks right, SpaceX may look like Amazon in 2001, a wildly overpriced stock that was still directionally correct. If it does not, this is the most expensive lesson in the history of TAM-driven valuations.

Three Businesses, One Number

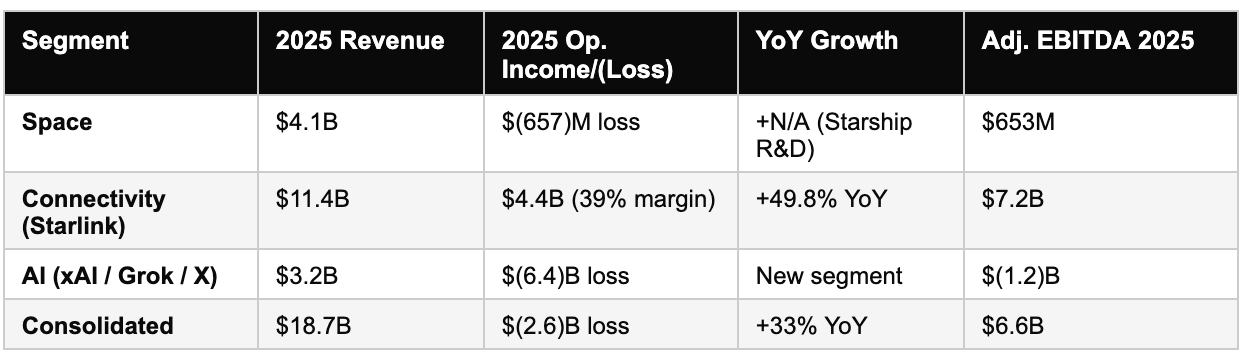

SpaceX is not one company. It is three very different businesses bundled into a single IPO price. We covered EBITDA in Episode 13 and Free Cash Flow in Episode 6 and both are essential lenses here, because GAAP profits and cash burn tell very different stories about each segment. The segment financials are detailed in “Management’s Discussion and Analysis,” beginning p.74 of the S-1.

Space: The Proven Engine

The original business and a genuine monopoly in the making with over 80% of global mass to orbit. A 99%+ mission success rate on Falcon 9 and Falcon Heavy. The company has spent over $15 billion on Starship (S-1 p.74, MD&A), and that investment has not yet produced commercial revenue. Starship is expected to begin payload delivery in H2 2026. As we covered in Episode 6 on Free Cash Flow, the challenge here is distinguishing maintenance capex from growth capex and at $15 billion of Starship spend, there is very little that qualifies as maintenance.

Connectivity: The Cash Machine

This is where the money actually comes from. Starlink delivered $11.4 billion in 2025 revenue, up 49.8% year-over-year. Operating income was $4.4 billion at a 39% margin. Starlink has10.3 million subscribers across 164 countries as of March 31, 2026 and subscribers doubled in 12 months, from 5 million to 10.3 million. As we discussed in Episode 13 on EBITDA, this is a business where the marginal cost per new subscriber approaches zero once the constellation exists. Starlink is currently subsidizing every other dollar SpaceX spends.

AI: The Burning Ambition

xAI, Grok, X, and COLOSSUS data centers were absorbed in February 2026. $3.2 billion in 2025 revenue. $6.4 billion in operating losses ($2.5 billion lost in Q1 2026 alone!). AI capex in 2025 was $12.7 billion which was nearly double the combined spending on rockets and satellites (S-1 p.74, MD&A -- AI Segment). This is the segment that turned a profitable company ($791 million net income in 2024) into a loss-maker ($4.94 billion net loss in 2025). The bull case requires believing this capital destruction is temporary and that the returns are ahead.

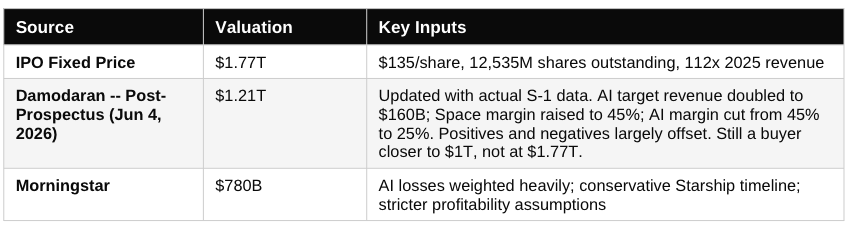

What Is It Actually Worth?

As mentioned at the top, and every headline make sure to remind us, the IPO price implies $1.77 trillion. Two of the most credible independent valuation voices have weighed in and I recommend reading them before making any decision. Here are those links:

Damodaran: “Revisiting the SpaceX Valuation: A Post-prospectus update”

Morningstar: “SpaceX: What it’s investors need to know about it’s enormous upcoming IPO”

I have summarized their findings below:

The spread between $780 billion and $1.77 trillion is not necessarily a disagreement about facts. It is a disagreement about which future you believe in. Damodaran’s base case is 31% below the IPO price, Morningstar is 56% below and both are serious analysts.

At $135 per share, you are paying 112 times 2025 revenue. There is no clean comparable. No existing public company has been priced this way at this scale, because no existing public company has attempted to simultaneously own the launch market, the satellite internet market, the AI infrastructure market, and the social media distribution layer (see above the largest actionable TAM in human history.”)

The Bottom Line

SpaceX is three businesses in one ticker: a proven rocket monopoly still funding its next-generation bet, a genuinely profitable satellite internet company growing at 50% per year, and an AI operation burning cash at a rate that would sink most companies. The IPO bundles all three at a multiple that prices in a future the core business has not yet delivered.

There is an old rule in valuation: conglomerates tend to trade at the multiple that befits their least attractive business. The market typically discounts complexity, penalizing the bundle versus the sum of the parts. By that logic, a company with a loss-making rocket division and a cash-incinerating AI segment should trade closer to an early-stage technology company than a mature infrastructure business and not at 112 times revenue.

But then there is the Elon effect.

Tesla has consistently traded at multiples that dwarf any auto company in history, not because of its car business, but because investors price in the full ambition of the platform (autonomous driving? robotics?). The same dynamic powered SpaceX’s private valuation from $350 billion in early 2025 to $1.77 trillion at IPO in under 18 months. Musk’s track record converts shared ambition into real capital, and real capital into real products. That premium is not irrational but rather it is a bet on one person’s ability to keep doing what he has already done.

One thing is certain: whether you buy SPCX or not, the index will bring it to you. Your passive portfolio is about to have an opinion on the multiplanetary future whether you form one or not.

Prepare accordingly.

Disclaimer: The views and opinions expressed above are current as of the date of this document and are subject to change without notice. Materials referenced above are provided for educational purposes only. Nothing above constitutes investment advice, a recommendation or an offer to sell, or a solicitation of an offer to buy, any securities or investment products. Always conduct your own due diligence and consult a qualified financial professional before making investment decisions.

Three businesses, three different quality profiles, one price. Starlink is genuinely profitable at 39% operating margins. The rocket business is pre-revenue on Starship. The AI segment lost $6.4B in 2025.

Traditional fundamental scoring breaks down entirely on a bundle like this. You can't run a quality screen on a company where 93% of the TAM didn't exist 12 months ago.

The passive ownership point is the most important practical takeaway. Whether you have an opinion on SpaceX or not, your Nasdaq index fund is about to form one for you.

Strong piece.

Since publication, the discussion has already moved into live price discovery. SPCX priced at $135, opened at $150, reached $176.45 intraday, and is now trading around $160.95. That puts the stock roughly 19% above the IPO price and implies about $2.1T of equity value if we apply the same share base.

Our BE Invested read is that your hierarchy is right.

Starlink is the cash engine. Launch is the strategic asset. AI/xAI is the valuation swing factor. Index inclusion is the technical demand layer.

The float point deserves even more attention now. The IPO sold about 555.6M shares. At $160.95, that is roughly $89B of initial tradable float. That number matters more for near-term index exposure than the $2.1T headline market value.

So the index debate needs precision. Passive funds may become buyers as Nasdaq fast-entry rules, float expansion, and future rebalances come into play. The first exposure is still float-adjusted. The larger mechanical demand arrives later, through lock-up releases and index methodology.

That is where the setup becomes difficult. The current price is already capitalising several outcomes at once: Starlink growth, launch dominance, Starship commercialization, AI infrastructure economics, float scarcity, and Elon execution.

SpaceX is an exceptional company. The valuation now requires exceptional execution across several businesses at the same time.

For us, the useful question is simple: how much of today’s price is operating value, and how much is scarcity, index demand, and story premium?