Politics Update: Three Countries... Same Mess.

“Plus ça change, plus c’est la même chose.” -- Jean-Baptiste Alphonse Karr, 1849.

The View From Three Passports

I am American, was raised in France and currently reside in London.

On Monday morning, Keir Starmer walked out of Downing Street and resigned. The UK is about to get its seventh prime minister in ten years. My first thought was not political, it was this: I have seen this movie before. Twice.

Because the same film has been running simultaneously in Paris and Washington. Different accents, different leaders, different excuses yet remarkably similar outcomes.

This special dispatch is an observation from someone who lives inside all three of these systems at once, who has watched them all struggle with the same problems, and who increasingly believes that none of them will escape cleanly anytime soon.

There are some obvious differences. Only one of these countries lacks air conditioning in most of its homes. Only one has a president who tweets at 3am. But underneath the surface noise, the macro picture is strikingly, almost uncomfortably, convergent.

Let me show you.

1. Political Instability: The Revolving Door

Ironically, the US is the most stable of the three. I hear you on the Tweeter in Chief, but hear me out. Its electoral architecture, fixed four-year terms, a two-party duopoly, and mid-term buffers makes leadership changes structurally harder. Since 2016 the US has had two presidents and congress has only flipped twice as well:

The House of Representatives

Jan 2017 – Jan 2019 (115th Congress): Republicans

Jan 2019 – Jan 2023 (116th & 117th Congress): Democrats

Jan 2023 – present (118th & 119th Congress): Republicans

The Senate

Jan 2015 – Jan 2021 (114th, 115th & 116th Congress): Republicans

Jan 2021 – Jan 2025 (117th & 118th Congress): Democrats — technically a 50-50 split, with VP Kamala Harris holding the constitutional tie-breaking vote

Jan 2025 – present (119th Congress): Republicans

By Westminster and Paris standards, the US looks like a model of stability, but “stable” is relative. I’ll admit, the US is not without its own structural problems, it’s just that the US system just hides them better.

France and the UK have had no such luck.

United Kingdom: 7 Prime Ministers in 10 Years

David Cameron (May 2010 – Jul 2016): resigned after losing the Brexit referendum he called

Theresa May (Jul 2016 – Jul 2019): resigned after failing three times to pass her Brexit deal

Boris Johnson (Jul 2019 – Sep 2022): forced out by his own party amid scandal and Partygate

Liz Truss (Sep 2022 – Oct 2022): 49 days, the shortest-serving PM in British history; outlasted by a head of lettuce

Rishi Sunak (Oct 2022 – Jul 2024): led Conservatives to their worst election defeat in over a century

Keir Starmer (Jul 2024 – Jun 2026): won a landslide promising “stability”; resigned 717 days later, removed by his own parliamentary party

and (most likely) Andy Burnham: former Greater Manchester Mayor

Three of the seven were removed by their own party, not by voters, one lasted 49 days, with an average tenure under 18 months. This is not a leadership problem, it is a governing problem.

France: 9 Prime Ministers in 10 Years

Manuel Valls (Apr 2014 – Dec 2016)

Bernard Cazeneuve (Dec 2016 – May 2017)

Édouard Philippe (Jun 2017 – Jul 2020)

Jean Castex (Jul 2020 – May 2022)

Élisabeth Borne (May 2022 – Jan 2024)

Gabriel Attal (Jan 2024 – Sep 2024)

Michel Barnier (Sep 2024 – Dec 2024): toppled by no-confidence vote, first since 1962

François Bayrou (Dec 2024 – Sep 2025): also toppled by no-confidence vote

Sébastien Lecornu (Sep 2025 – present): resigned after 26 days then reappointed; shortest initial tenure in Fifth Republic history

The National Assembly has been ungovernable since Macron lost his majority in 2022. France has averaged one new prime minister every 13 months since 2016. Macron’s domestic approval rating stands at 18%. Lucky for him, he is constitutionally barred from running again in 2027. The current PM is functionally a caretaker in a country without a functioning majority.

The common thread across all three is not bad leaders. It is a collapse in the centrist governing consensus that held the Western world together for 30 years. The voters are not satisfied with the offer and the leaders feel it acutely. The markets are starting to as well.

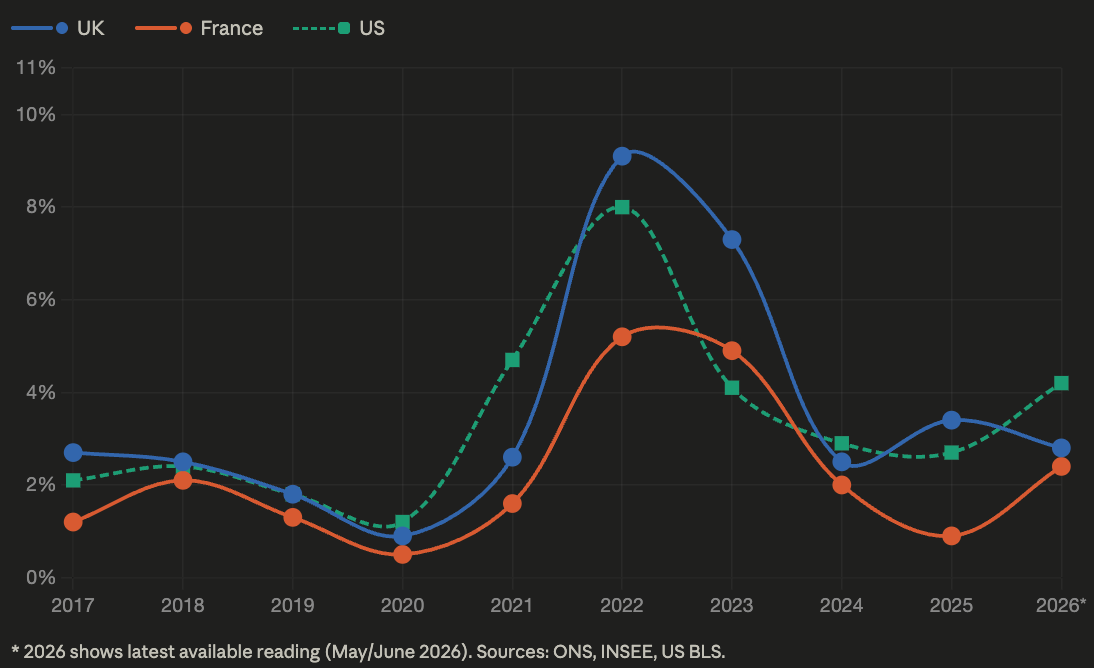

2. The Cost of Living: Same Storm, Different Timing

Three inflation experiences that followed almost identical trajectories.

The story follows the same script:

Low inflation through 2019.

Covid killed demand and killed prices in 2020.

Stimulus and supply-chain chaos lit the fuse in 2021 and the explosion hit in 2022. By October 2022 UK inflation hit 11.1% while in the US CPI hit 9.1%. France, thanks to government energy price caps, cushioned the blow to 5.2%.

After steep falls in 2023-2025 all three countries are seeing CPI moving back up, pushed by the Iran war energy shock.

None of these countries are at their central bank’s target and more concerning, none are on a clear path back to target. France looks the calmest on inflation but carries the heaviest political risk premium in its bond market.

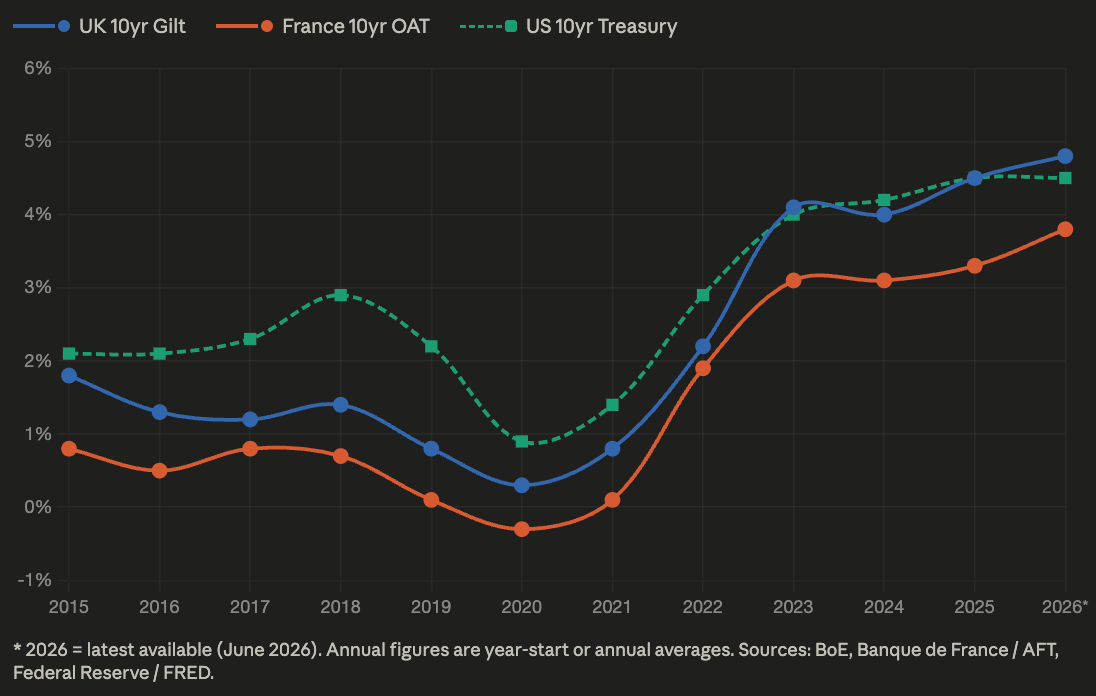

3. Bond Yields: When Did We Last See These Levels?

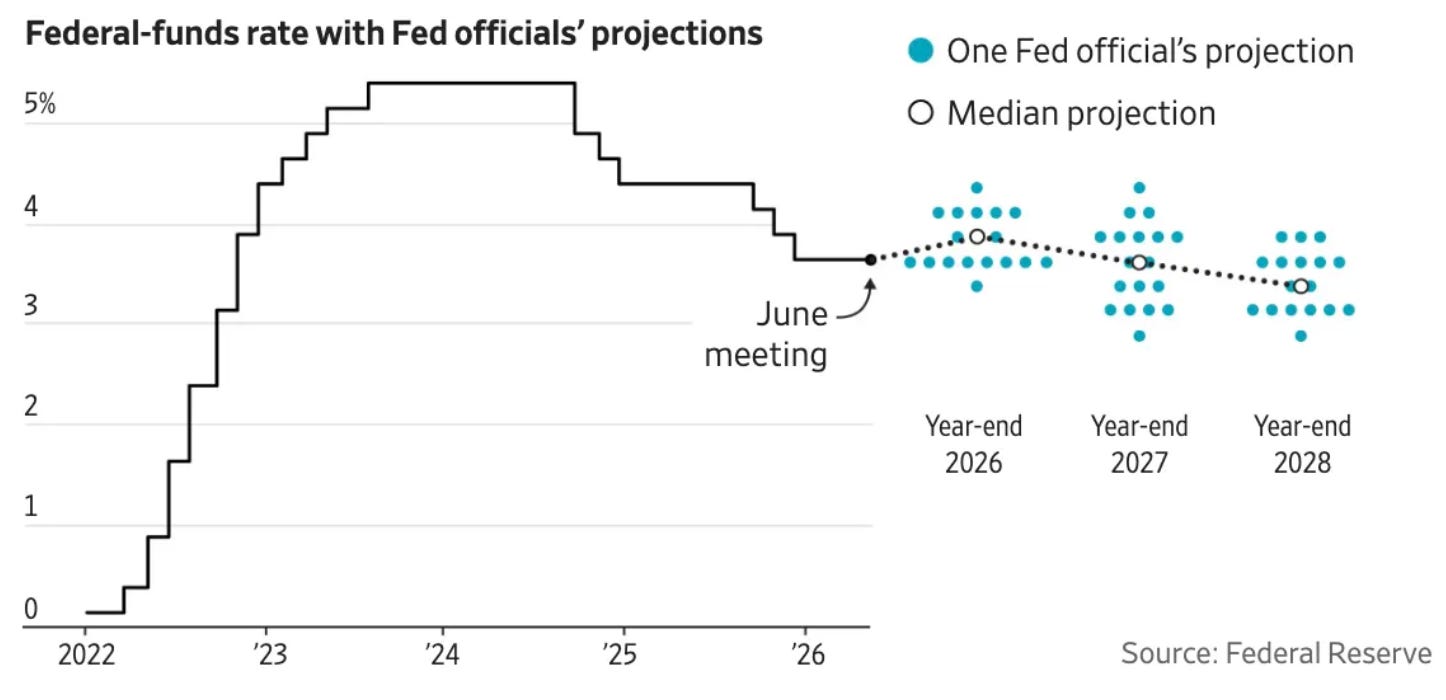

Central bank policy rates get the headlines, with the ECB hiking rates in mid June and Kevin Warsh’s Fed meeting a few days later. But the 10-year sovereign benchmark (the UK gilt, the French Obligations Assimilées du Trésor or OAT, and the US Treasury bond) is the number that actually prices your mortgage, your government’s borrowing costs, and the discount rate on every investment in the economy. And all three are telling the same story.

The UK 10-year gilt yield is at its highest levels since July 2008, the French 10-year OAT yield is hovering near its highest levels since June 2009 and the US 10-year yield is close to levels last reached in June 2007. This is largely driven by inflationary pressures from elevated energy costs and heightened geopolitical tensions in the Middle East.

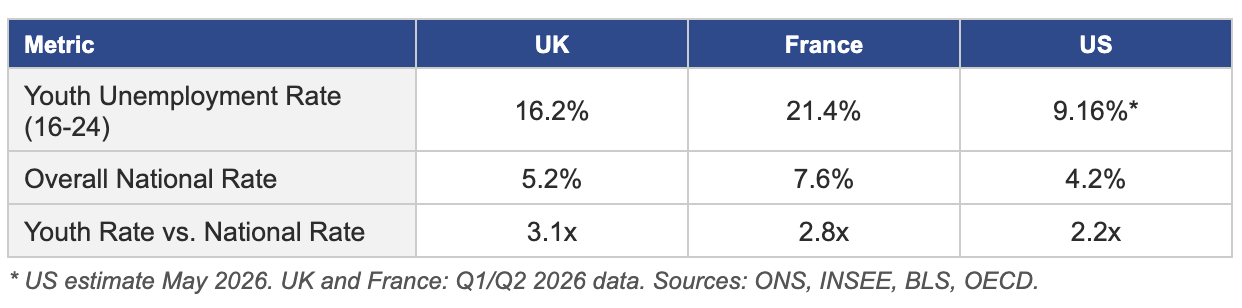

4. Youth Unemployment: The Generation Left Behind

The next generation is the quiet crisis inside the more visible economic numbers. Youth unemployment is simultaneously a social, economic, and political time bomb.

The US number looks the best of the three but deserves context. At 9.2%, US youth unemployment is still more than double the national rate and for Black and Hispanic youth it runs considerably higher. The structural problem is the same across all three countries: a labor market that is bifurcating between knowledge workers and everyone else, with young people disproportionately stuck on the wrong side.

France’s 21.4% is the number that should alarm the most. One in five young French people looking for work cannot find it and goes a long way towards explaining the rise of the National Rally party. When a generation feels economically excluded, they vote for the party that promises disruption.

The UK’s 1.01 million young people classified as NEET, not in employment, education, or training, is the first time that figure has crossed a million since 2013. The pandemic created a generation of economically inactive young people.

5. Housing: The Ladder Nobody Can Reach

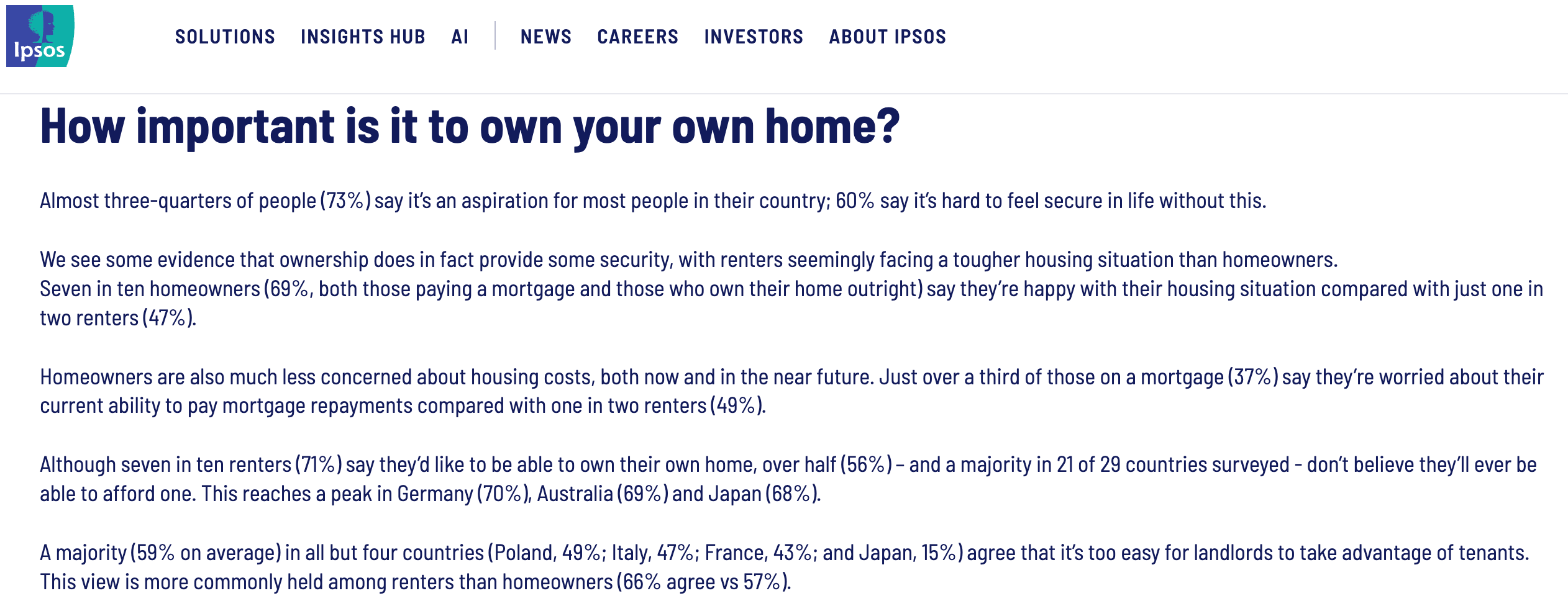

Buy a home, build wealth, and pass it to your children. This was the Western compact for three generations. It has broken down in all three countries simultaneously.

An Ipsos global survey puts a number on the despair: 73% of people surveyed said they want to own their own home. 56% of renters do not believe they will ever be able to afford one.

France is the relative bright spot.

Government intervention in energy prices cushioned the inflation hit, tenant protections are among the strongest in Europe, and house price corrections since 2022 have improved affordability on the margins. Only 43% of French renters say landlords can easily take advantage of them, the lowest in Europe after Japan.

The UK is the worst of the three on housing relative to wages.

Median house prices in England and Wales are close to nine times median earnings in many regions. Mortgage rates that tripled in 18 months have locked out first-time buyers. UK house price growth is forecast at just 1.5% in 2026, down from earlier projections of 3%. Prime central London is expected to fall 2%. The dream of homeownership is not just deferred for many young Britons, it may be permanently out of reach.

The US sits in the middle.

Rate hikes took 30-year fixed mortgage rates from below 3% in 2021 to above 7% by 2023, collapsing affordability overnight. Rates remain elevated today at over 6% and the inventory shortage kept prices high even as rates rose, creating the worst of both worlds.

The common factor across all three is the same: supply has never caught up with demand. Why is this?

Building homes is politically difficult.

Existing homeowners are the most reliable voters and the NIMBY effect is real.

Housing supply has structurally lagged for 20 years in all three economies.

That gap is not closing quickly.

6. Immigration: The Fault Line That Changed Everything

Immigration did not just become a political issue in the past decade. It became “the” political issue and it reshaped the governments of all three countries in ways that are still playing out.

In the UK, Brexit was fundamentally an immigration argument dressed in the language of sovereignty. The official Vote Leave slogan ‘Take Back Control’ was not about trade law. It was about who comes through the door. It worked and it set off a chain of political and economic consequences that has not ended a decade later.

In the US, Trump’s first election in 2016 was built on a simple, effective message about the southern border (“Build The Wall”). By 2024, immigration had become the top issue for a majority of Americans heading into the election, with Democrats seen as fundamentally weak on the issue. Trump won. The numbers since tell an interesting story: deportation crackdowns have paradoxically made Americans more pro-immigration, not less. Gallup found 79% of Americans now say immigration is a good thing for the country, a record high. When enforcement became visible and aggressive, sympathy for immigrants surged.

France has its own version. The National Rally is polling at 35% nationally. Although Marine Le Pen faces a suspended sentence that may bar her from public office, her number 2, Jordan Bardella, tops every political approval chart in the country with a 35% rating. A January 2026 CSA poll found 67% of French voters support a two-to-three year pause on all new family reunification visas and work permits. Yet when the same voters are asked about their local community, immigration drops to seventh place as a concern, behind cost of living, healthcare, housing, and jobs.

The Synthesis: Why None of Them Can Fix It Quickly

I moved between these three countries over the past five decades. What strikes me most is not how different the three systems are, it is how similar the grievances are. Cost of living, housing, youth locked out of economic participation with immigration used as a proxy for all of the above. I have not even gotten onto the topic of national debt, which is causing all sorts of problems for the political leaders in these countries.

The political instability in all three countries is the output, not the input. Leaders keep losing because the problems are not solvable inside a single electoral term. And voters, quite rationally, keep punishing leaders who overpromise. The centrist promise of managed competence has been tested and found wanting.

The solutions are long-horizon and politically painful. Build more housing, invest in youth training, reform energy infrastructure, manage immigration with clear rules and adequate processing. These are not secrets and every think tank in every capital has published these recommendations. The political will to execute them consistently across multiple election cycles has not materialized in any of the three and is unlikely to do so given the current state of affairs.

Which brings me to the most urgent unanswered question of 2026:

Which of the three will go furthest at the 2026 World Cup?

Because frankly, on current form, that might be the only competition any of them has a realistic chance of coming out ahead. On current form, football might be the one arena where any of them can claim a clean win.

Whoever lifts the trophy, the economic scorecards above will still look the same on the Monday after the final. Winning a World Cup is easier than building affordable homes.

Stay Curious and Keep Learning. Investing. Thriving.

DISCLAIMER: The content in this newsletter reflects the views of the author as of the date of publication and is subject to change without notice. It is provided for educational and informational purposes only and does not constitute investment advice or an offer to buy or sell any security. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. Please consult a qualified financial advisor before making investment decisions. World Cup predictions carry equivalent risk.

Excellent observations!